Live & Online Business Conference - 31 March & 1 April 2026 (workshop 30th March)

Live & Online Business Conference - 31 March & 1 April 2026 (workshop 30th March)

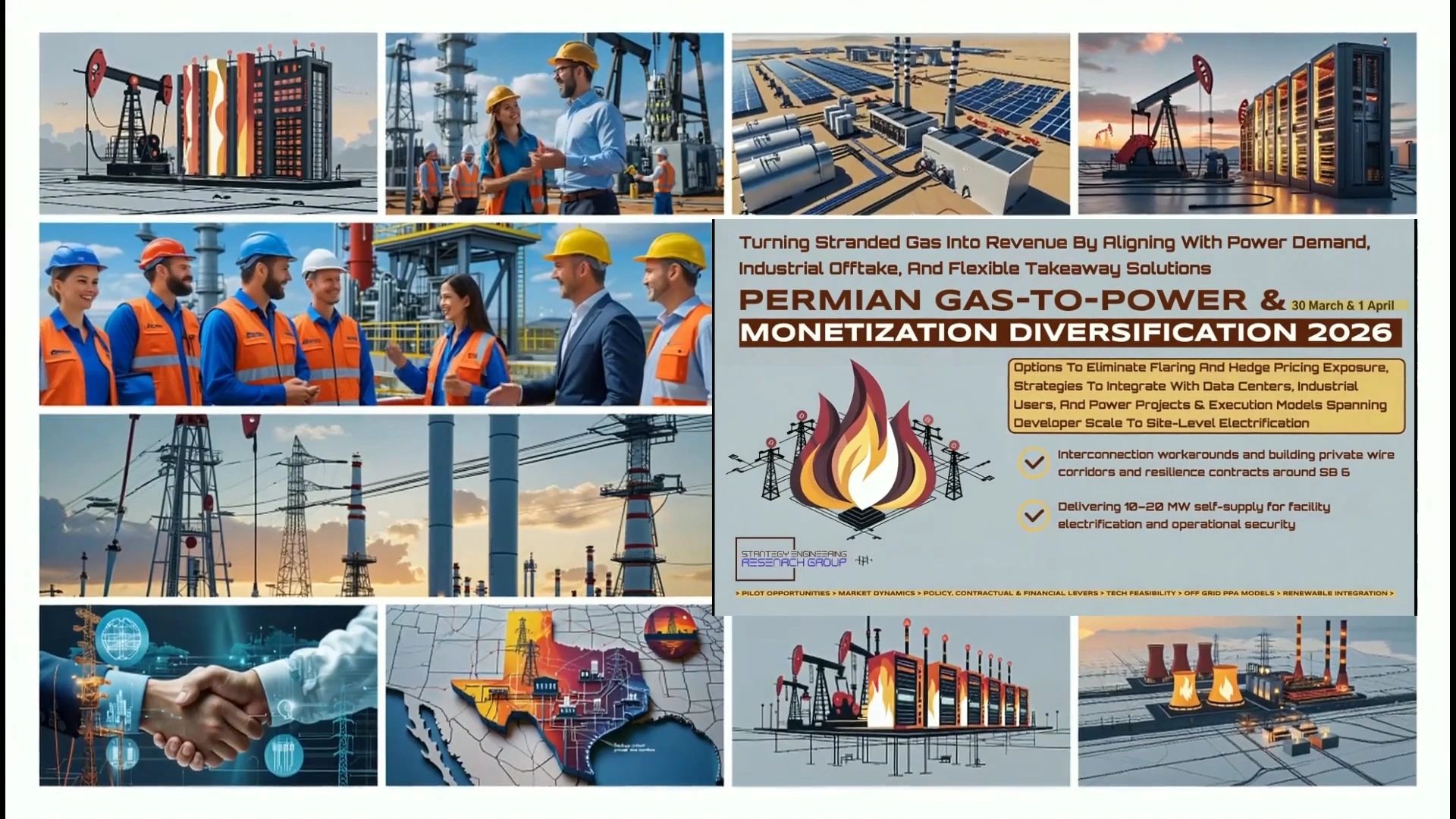

While operators are regulated against flaring billions of cubic feet of gas in the Permian, ERCOT faces record demand from data centers scrambling for backup power. This conference is where those two realities finally meet.

The first forum to unite executives and operators across the gas-to-power chain — from producers and midstream to grids, buyers, financiers, and regulators.

From upstream to hyperscale data centers, this forum connects every link in the chain to make gas monetisation real.

The focus goes beyond turbines and pipelines — into deal structures, PPAs, hedges, ROI frameworks, and investor confidence.

It’s not just for majors. Independents get clear pathways too — partnerships, pooling, onsite power, innovative finance.

The outcome: a forum that is strategic and practical. Where every stakeholder, from upstream operators to hyperscale data centers, leaves with clarity on what’s next and who to potentially partner with.

Reserve your seat now — places are limited.

Two crises, one room: billions of cubic feet of stranded and flared gas on the supply side, and explosive data-center and industrial load on the demand side. This is the first event designed to connect them.

For operators, "gas monetization now ranks just behind capital discipline and free cash flow" on the 2026 priority list. At the same time, ERCOT is bracing for record demand from hyperscale data centers and heavy industry.

Consider these data points and facts.

ERCOT recently raised its forecast for 2030 load/peak demand growth by about 40 GW compared to its previous forecast. Meaning that the total 2030 forecast peak load is around 152 GW under the newer heightened assumptions.

Over 200 independents in the Permian alone face takeaway and flare challenges but lack scale. Partnerships and pooled projects are critical.

U.S. data center power demand is projected to double by 2030, with Texas leading in new hyperscale builds. Backup and resilient supply are top priorities.

And yet…

Over 200 independents in the Permian alone face takeaway and flare challenges but lack scale. Methane emissions rules are tightening in 2026–27, raising costs for flaring and creating urgency for alternative solutions.

As one operator recently put it

‘We’re burning cash with every flare while power prices spike across ERCOT — we urgently need solutions now.’”

The conference agenda is built to serve these priorities, giving executives not only peer insights but also the contractual, technical, and practical frameworks needed to advance monetization strategies immediately.

What Operators Are Really Learning—ERCOT Delays, Permit Bottlenecks, Tech Trade-Offs, and New Ways to Link Gas Producers with Power Buyers

Sessions will cover gas monetization, interconnection planning, technology comparisons, and structured offtake deals—including behind-the-meter PPAs.

“Our biggest risk is power security. If we can align with operators and developers on resilient supply, it changes everything.” — VP Energy Strategy, Texas Hyperscaler Ai Data Center

The agenda showcases short-term monetization models that bridge operators through to the LNG era, including behind-the-meter supply, captive power projects, and fast-tracked distributed solutions.

Smaller operators face flare penalties but lack pathways. Partnerships, pooled projects, and onsite generation are essential. This forum looks at options for junior and mid-size operators alongside majors.

Unpacking solutions such as:

A select group of senior leaders is guiding the agenda to ensure it reflects real operator and buyer priorities.

· Independent E&Ps across the Permian

· Midstream operators and project developers

· ERCOT and ISO market leaders

· Hyperscaler energy teams

· Infrastructure investors and lenders

· OEMs and EPCs

AGENDA HIGHLIGHTS

Flare To Firm Power → How Producers And Hyperscalers Align On Reliable Supply

ERCOT Interconnect → Cutting Through The Backlog With Regulators And Developers

Financing Monetisation → Ppas, Hedges, And Blended Finance Models That Work

Small Operator Pathways → Pooling, Partnerships, And Onsite Power

ESG Pressure As Opportunity → Monetisation As Compliance And Reputation Strategy

Example Talks, Agenda Teasers & Case Studies Include

Operator/Buyer/Finance/Regulator Sessions Built Around Bankability And Interconnect Feasibility (Reflecting ERCOT Large-Load Growth And Queue Friction)

Collaborating To Address Risk When Bring Molecules To Megawatts—E&P + Midstream + OEM + IPP + Buyer + Capital

Pairing AI Hyperscalers With Operators, Developers, And Capital To Convert Load Growth Into Reliable Capacity

Panels Featuring Regulators And System Planners Sit With Operators, Financiers, And Hyperscalers To Clear Pathways Against ERCOT’s Large-Load Queue And Multi-Year Interconnection Timelines

Strategies From Regulators, Grid Operators, And Developers To Unlock Capacity Faster

Practicalities For Getting Gas-Fired Projects Permitted

How Hyperscalers Structure Behind-The-Meter PPA’s

Pooling Resources For Midstream Tie-Ins, Compression, Or Power Hubs

Building Commercial Models That Pay Back Within 12–24 Months

Cost Effective Approaches For Converting Flared Gas Into On-Site Power

Unlocking ERCOT for Permian Gas Projects

How this differs from other initiatives

Conferences have yet to put Permian upstream operators, OEMs, financiers, regulators, and large-load buyers into one deal room to clear interconnects, PPAs/hedges, and ROI.

This summit does exactly that—matching Permian gas realities with ERCOT large-load growth and the capital to make it bankable.

Other regions around the US take note - What gets solved here in Texas sets the template nationally for gas monetisation, flare reduction, and large-load reliability across the whole United States and Canada.

Speaker Announcements Coming Soon

Confirmed operator, investor, and regulator speakers will be released in the coming weeks. Expect perspectives from:

· Major and independent upstream producers

· ERCOT and state energy regulators

· Hyperscale data center energy buyers

· Infrastructure and project financiers

· Technology innovators (generation, CCUS, digital controls)

Who You’ll Meet

The only event bringing the full value chain into one room:

Operators (Majors & Independents) → monetising flared and stranded gas

Midstream & Developers → gathering, takeaway, and flexible generation

Grids & Utilities (ERCOT, ISOs, Municipals, Co-ops) → ensuring reliability and capacity

Power Producers & IPPs → delivering modular, hybrid, and distributed projects

Microgrid & DER Developers → redefining site-level resilience

Data Centers & Hyperscalers → securing firm, lower-carbon supply

Industrial Buyers (Steel, Cement, Fertiliser, Chemicals) → cutting exposure and locking in flexible supply

Emerging Offtakers (Hydrogen, Ammonia, LNG Bunkering) → expanding demand pathways

Investors & Financiers → making projects bankable

Regulators & Policymakers → shaping frameworks and clearing bottlenecks

OEMs & Service Providers → turbines, modular plants, CCUS, digital controls

Traders & Risk Managers → structuring PPAs, hedges, and risk exposure

ESG & Carbon Specialists → compliance and emissions management

What You’ll Gain

Operators: real monetisation options, from pooled projects to onsite power

Investors: access to bankable projects and credible partners

Buyers: reliable, lower-carbon backup supply to meet surging demand

OEMs & Service Providers: visibility in a deal-driven setting, not a trade show

Regulators: a platform to align market design with real project needs

The value doesn’t stop when the meeting ends. Every discussion feeds into a post-conference insights report capturing ROI models, project frameworks, and regulatory signals. Attendees also join a dedicated follow-up network to continue building partnerships.

“Capital is there, but ROI models are not. We need operators, OEMs, and buyers in the same room to make these projects bankable.” — Infrastructure Fund Partner

“Rules can enable projects, or stall them. This kind of dialogue is exactly what’s needed to align policy with market needs.” — State Energy Commissioner